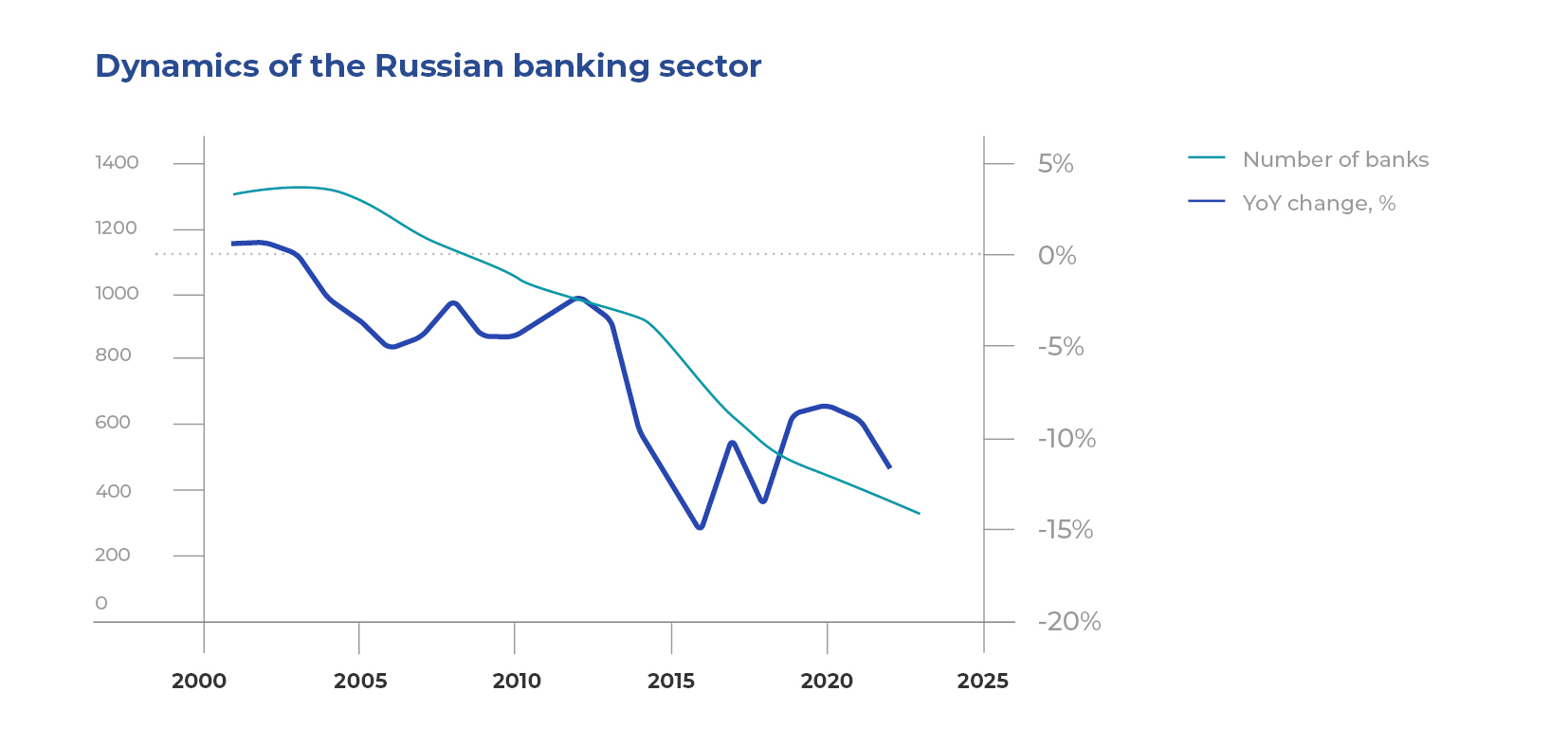

Despite a more than two-fold reduction in the number of banks over the past decade and a significant consolidation of the banking sector, there are still more than 300 medium-sized and small financial institutions operating in Russia¹.

Their combined assets amount to RUB 25–30 trillion, or about 18–22% of the total size of the Russian banking market.

Experts of the Yakov & Partners Financial Practice analyzed the current state of small and mediumsized banks operating in Russia to identify the market trends and the direction of the evolution of business models in the banking sector, as well as to assess the risks and opportunities stemming fr om the current macroeconomic and geopolitical environment.

Current market situation and its challenges

The Russian banking market is represented by corporate and retail financial institutions, with the overall ratio of corporate to retail loans standing at 2.2 to 1. As to the structure of customers’ funds, the ratio stands at 1.3 to 1 – also in favor of legal entities2. The specific character of the operations of these institutions determines their main goals and the way their business models evolve. Both the corporate and retail segments of the banking business are impacted by multiple global trends, with Open Banking being in the lead as it is gaining traction in the banking market.

Open Banking is the practice of allowing third parties access to customers’ banking data subject to their consent. For instance, banks will get access to information on customers’ current account balances and transaction activity in other banks.

The introduction of Open Banking is set to transform the banking market: as competition will intensify, new products and players will enter the market, and the ways banking services are delivered to the end consumer will change. In 2022, the Bank of Russia published "Open APIs in Russian market: Bank of Russia’s concept". This document describes the options and a step-bystep plan for Open Banking implementation in Russia3. Fr om 2024 on, some banks will be obligated to open up part of their APIs, so banks should start preparing their infrastructure and review their business processes and longterm development strategy as early as this year in order to be well-equipped to face the new developments. The new approach will significantly increase the amount of data based on which the creditworthiness of customers is assessed, and it will have impact on market competition. This way, small and medium-sized players will get access to the transactional data of retail customers of other banks, which will make luring customers away fr om competitors easier. Similar changes will occur in the corporate segment as banks will gain more information about companies to judge their creditworthiness.

The current geopolitical situation has significantly hampered the ability of Russian banks to carry out international settlements in "unfriendly" jurisdictions, prompting customers to flee to those banks that face no difficulties in this respect. According to Expert RA Agency, those banks that ranked 11th to 100th in terms of assets in 2022, performed 10% better than the year before. This could be chalked up to the churn of customers from large lenders, many of which incurred losses4. 2022 and early 2023 saw an acceleration of the trends that lead to changes in both the products that facilitate international settlements and the logic of those transactions as such, as cryptocurrencies and blockchain technology are increasingly more often used in international trade.

At the same time, macroeconomic uncertainty complicates the development of lending business, leading to shorter lending periods. Banks need not only to restructure their portfolios, but also to revise the approaches to assessing credit risks and determining the covenants. As scoring and rating models are losing their relevance, their mechanics and target values require an overhaul. For corporate banks, this trend will further complicate the assessment of customers’ long-term investment projects.

The Bank of Russia considers it expedient to launch the Open Finance model (option 1) and later transition to the Open Data model (option 2).

The nitty-gritty of the corporate banking sector

The trends and main objectives pertaining to the development of corporate banks and business units of universal banks responsible for serving legal entities are governed by the trajectory of Russia’s economic development over the past 25–30 years. These objectives could be classified into internal and external, with the latter being especially relevant for medium-sized and small players. By internal objectives we mean the choice of business and organizational models, allocation of responsibility centers, giving authority to business units and motivating the employees. In turn, external ones include ensuring strong performance in a highly competitive market, identifying new customer segments, expanding the product offering, and choosing the best way to create value for the customer.

The described trends and objectives concern all banks, but for some of these organizations those trends create additional risks and challenges. Medium-sized and small corporate banks are subject to the greatest risk as they tend to have highly concentrated loan portfolios and an insufficient commission income / OPEX ratio. Lower quality of risk of the main borrower would entail higher reserves and a decline in the interest income, which, along with a low commission income, could lead to significant losses.

To respond to this challenge, banks need to adopt a new approach to business model development and take a number of measures to increase internal performance. In particular, they should reconsider classic product-oriented methods of operation in favor of "customercentric" ones, apply advanced customer analytics tools to risky and risk-free products, transform customer journeys for different services, introduce new metrics, and design advanced CRM systems and dashboards to build a 360-degree view of the customer.

These measures will help increase the transaction activity of customers and diversify the loan portfolio. The model in which all operating expenses are offset by risk-free transactional revenue, and the ratio of profit from risky products to profit from risk-free ones is 60 to 40%, has traditionally been considered the benchmark.

The recent emergence of such niche players as digital fintech companies only fueled competition in the market. They create "anchor" products, change the logic and increase the speed of value creation for the customer, which allowed them to win a significant share of transactional revenues from "classic" banks. At the same time, the quality of service is constantly improving, and to remain competitive in the transactional business, conventional corporate banks have to meet the new standards. Among the external factors that create considerable challenges for the market players, is the new market environment, which prompts them to tailor their value proposition to customer needs even faster. Those banks that have not been hit by sanctions or cut off from the SWIFT system, as well as subsidiaries of foreign credit institutions, have the opportunity to solve an important problem for their customers by modernizing the services related to international settlements and transforming the FEA function. What’s more, they could become the champions of brand-new alternative methods of settlements. Meeting customers’ demand for high-quality international settlement services will become an "anchor" product that could be followed by others.

Amidst change, new customer segments and opportunities are emerging that should be leveraged in order to sustain or ramp up business. Any platform that can connect commercial transactors and meet their funding needs will do the trick. Relying on such solutions, banks can also increase their liabilities, while additional commission products will help provide a higher return on shareholder equity.

Yet another approach would be to focus on a single product to increase the customer base by accelerating value creation for the customer and expanding the "delivery" channel. Many small and medium-sized players are yet to take full advantage of the potential of omni-channel customer service, although given the upcoming transition to open protocols (API), such services are becoming particularly relevant.

Retail banking also offers a number of unique challenges and opportunities.

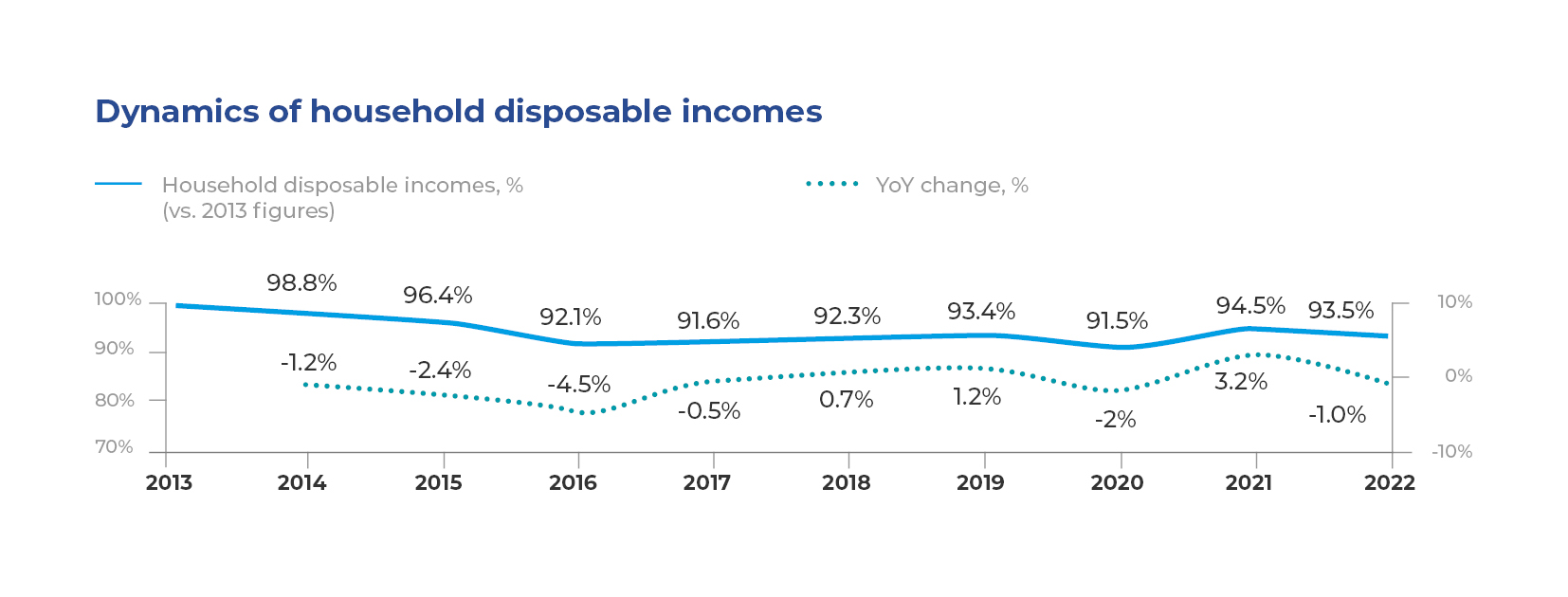

- Should real household earnings continue to decline, it could hit the creditworthiness of retail customers and result in a higher share of NPL. The cumulative decline in real disposable income over the past 10 years stands at 6.5%, although during some crisis years the decline was as high as 5%⁵. If the negative trend persists amidst the uncertainty, consumption is very likely to drop, which would entail a slump in lending business.

- The digitalization of customer journeys and development of the rapid payment system created a situation wh ere customers are able to switch fr om one bank to another with little or no expense. This accounts for the high turnover rate: according to our estimates, the average customer is served by at least 2.5 banks. While attracting customers depends largely on the rates and efficient advertising, retaining them hinges on the quality of day-to-day service and the convenience of digital channels.

- In recent years, marketplaces have entered the financial market and are now stepping up their efforts in this area. Yandex Market, Wildberries, and Ozon acquired banks and issued their own debit cards back in 2022. Those cards give customers additional benefits when paying for goods on those sites and can also be used to pay for any other purchases. If customers keep using those cards to pay for goods on marketplaces, "classic" banks stand to lose RUB 20 to 50 billion in net operating income⁶. In addition, this will create significant problems for the lending business of incumbents, as marketplaces can develop targeted value propositions in certain product niches thanks to their extensive active customer bases and multiple points of contact.

- The introduction and popularization of the digital ruble may result in an outflow of funds from commercial banks, as the digital rubles will be stored in the Central Bank. This, in turn, will cause an increase in the cost of funding and a loss of commission income from payments.

In the retail segment, the described trends pose the greatest risks to medium-sized and small monoline lenders that focus on unsecured consumer loans and generate rather low commission incomes from daily transactions (or none at all). Increased transaction activity in everyday banking leads to larger balances on customers’ current accounts and a lower cost of funding. As the experience of multiple banks shows, the average balance per customer directly depends on the number of transactions.

As exemplified by one of the banks we analyzed, a 15–20% increase in transaction activity can double the balances on current accounts. What’s more, the churn rates among transactionally active customers are several times as low as among the rest. This is especially important in terms of customer retention, given that the cost of switching to another bank is very low. At the same time, lending monoliners will have more transactional data on their customers, which will allow them to better assess their creditworthiness when selling "anchor" credit products.

The earnings of lending monoliners are more than 85% dependent solely on loan disbursements and payments7. If the economic activity and loan portfolio turnover decline, banks face high risks of losses. They should restructure their business models and start developing transactional products in order to reduce the dependence on their lending business.

The first step is to analyze the customer base, identify the root causes of low transaction activity and find ways to increase it. For example, if the bank has a young customer base, it would make sense to engage customers through gamification techniques, as games create additional non-financial incentives for transactions.

Regardless of the type of customer base, it is important to launch "linking" types of payment that will become "anchors" for the users. Those include NFC payments with a tokenized card, payment aggregators, or biometric payments. Activating these payment methods requires that users perform a certain action, but the more accustomed they become to using those methods, the less likely they are to give up on this new and convenient habit. For example, once a card has been linked to a taxi aggregator app, users tend to stick to this payment method for quite a while. "Linking" types of payments can also be popularized through financial rewards, such as cashback or partner discounts. In addition, banks can introduce special transactional products, such as region-linked social cards.

Transactionally active customers could be offered more favorable terms for "anchor" loan products, for instance a lower interest rate on consumer loans if there are transactions exceeding a certain value. At the same time, in light of the recent trends, banks need to prepare for the launch of the digital ruble and consider developing transactional products based on the new digital currency with an option to "mark" the target categories and implement smart contracts.

While developing a strategy to increase transaction activity, retail monoliners should make sure that they will be able to sustain breakeven performance even in case the Central Bank imposes restrictions on the sale of insurance products in addition to credit ones.

Banking market development prospects

In the current environment, medium-sized and small banks may encounter serious problems. Based on our estimates, the takeaways from the past crises, and the current circumstances, we can expect that 65% to 80% of small and medium-sized banks will disappear over the next 10 years8. The largest banks will continue their digitalization and service improvement efforts, leading to further concentration of the banking market. Major players will continue to strengthen they positions, undermining the competitiveness of small and medium-sized banks in their customer and product niches. Large banks will expand their regional presence wh ere local players are strong, acquiring medium-sized and small companies or squeezing them out of the market. As the banking sector is systemically important, such risks will have wider economic consequences. Our analysis of the business models of medium-sized and small banks shows that they could gain an additional RUB 300– 400 billion in annual profits if they go through with the transformation and improvement of their business models. Thus, in order to maintain their positions and keep developing under the new circumstances, it is essential that all medium-sized and small banks establish a new development vector.

Transforming a business model is no mean feat. Shareholders and board members need to thoroughly analyze to what extent their bank's business model is developed compared with competitors. In particular, they should assess the maturity of all credit and transactional products and other aspects of the business model, e. g. the quality of CRM. It is equally important to assess the maturity of customer journeys: the availability and development of necessary service channels, the sophistication of remote banking services, the quality of customer onboarding, etc. And in order to do business successfully, banks need to adjust their organizational models and supporting mechanisms accordingly. Among other things, they need to improve the quality of the credit pipeline, infrastructure, customerfacing and back-office processes.

Assessing the maturity of these elements will help banks determine wh ere the greatest potential lies and wh ere to focus their efforts for successful long-term development.

1 Bankig Sector, Bank of Russia, 2023

2 Development of the Russian banking sector (in brief), March 2023

3 Open APIs in Russian market: Bank of Russia’s concept, 2022

4 2023 banking sector outlook: Olympus has fallen, RAEX, 2023

5 Real household disposable incomes in the Russian Federation, Federal State Statistics Service, 2023

6 Inhouse estimate by Yakov & Partners, 2023

7 Inhouse estimate by Yakov & Partners based on published banks' reports

8 Inhouse estimate by Yakov & Partners, 2023